3. Bridge Loans

Best for Value-Add or Time-Sensitive Opportunities

4. Alternative & Private Financing

Best for Unique, Complex, or Creative Deals

Not every deal fits inside a bank’s box.

Alternative financing in Texas may include:

- Private lenders

- Hard money loans

- Seller financing

- Equity partners

- Family offices

- Faster approvals

- Flexible underwriting

- Creative structures

- Useful when banks decline deals

Higher interest rates and fees.

Land purchases, transitional properties, or projects needing nontraditional structuring.

Owner-User vs Investor Financing Strategy

Understanding your role changes everything.

If You Are an Owner-User:

- SBA 504 is often the most capital-efficient option

- Focus on long-term stability

- Preserve cash for business growth

- Traditional bank financing for stabilized properties

- Bridge loans for repositioning strategies

- Private capital for speed or complexity

Key Factors That Affect Your Loan Approval in Texas

Regardless of loan type, lenders evaluate:

- Creditworthiness

- Liquidity

- Net worth

- Debt service coverage ratio (DSCR)

- Property cash flow

- Market conditions

- Experience level

Texas remains one of the most active commercial real estate markets in the country, but underwriting standards still matter.

How to Choose the Right Financing Option

1. Is this a long-term hold or short-term reposition?

Your timeline drives your financing. Long-term holds favor stable, lower-rate loans, while short-term value-add deals may require flexible, short-term financing like bridge loans.

2. How much capital do I want to keep liquid?

Higher down payments can lower risk and payments, but tying up too much cash may limit your ability to handle surprises or pursue other opportunities.

3. Do I need speed or stability?

If timing is critical (competitive deal, distressed asset), faster financing may matter more than rate. If not, slower, more stable financing often provides better long-term terms.

4. Is the property stabilized?

Stabilized properties (with consistent income) qualify for traditional loans. Properties with vacancy or issues may require bridge or alternative financing first.

5. What is my exit strategy?

Are you planning to refinance, lease-up, or sell? Your loan should align with that plan — especially if you’re using short-term financing.

The right loan should align with your investment timeline — not just offer the lowest rate.

Final Thoughts

There is no single “best” financing option for commercial real estate in Texas — only the one that best aligns with your strategy.

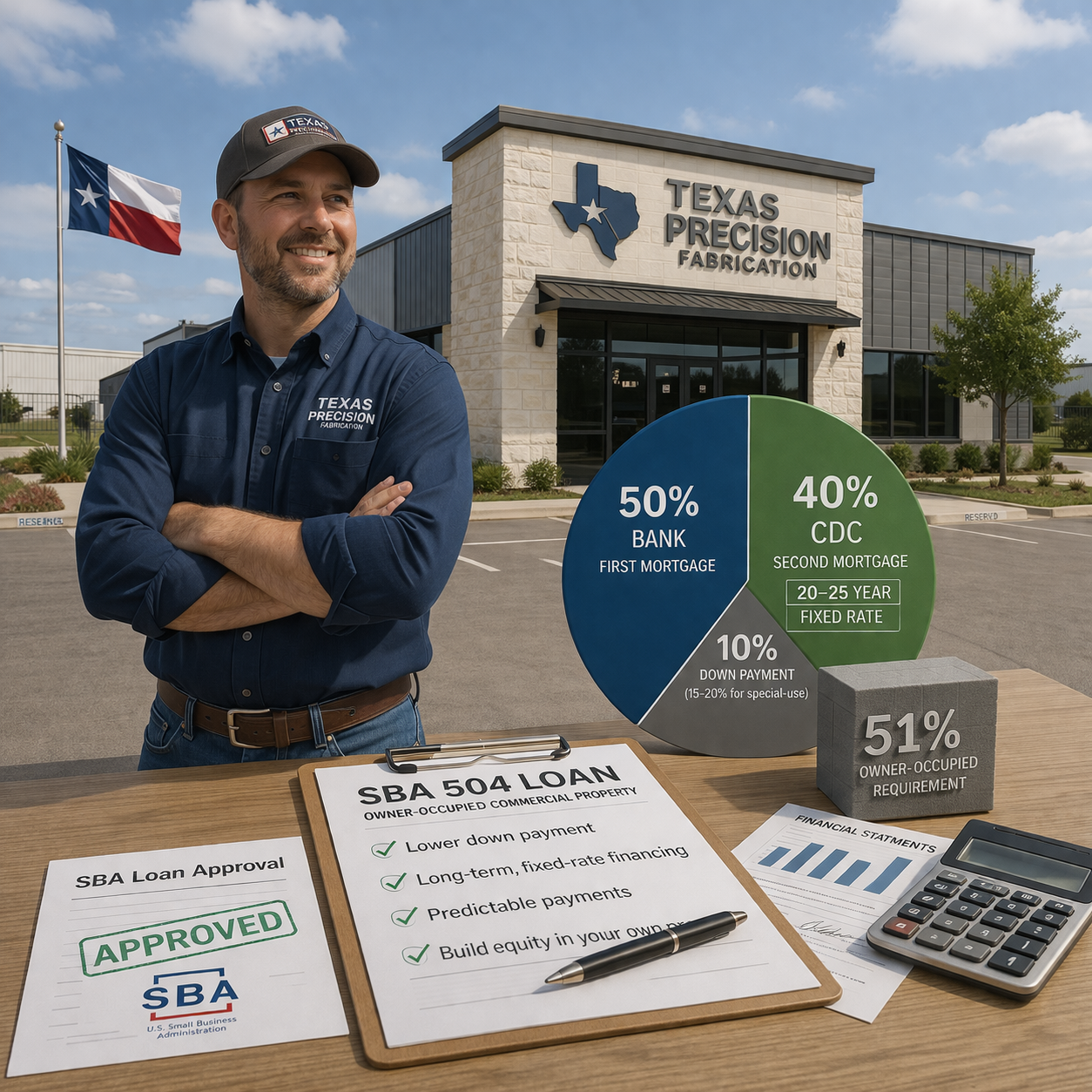

- SBA 504 loans help business owners build equity with less cash down.

- Traditional mortgages offer stability for investors.

- Bridge loans create speed and flexibility.

- Alternative financing unlocks complex opportunities.

Understanding these tools gives you leverage — not just in negotiations, but in long-term wealth building.

If you're evaluating a commercial purchase in Texas and want guidance on structuring financing that supports your investment goals, working with

experienced commercial real estate professionals can help you move forward with clarity and confidence.